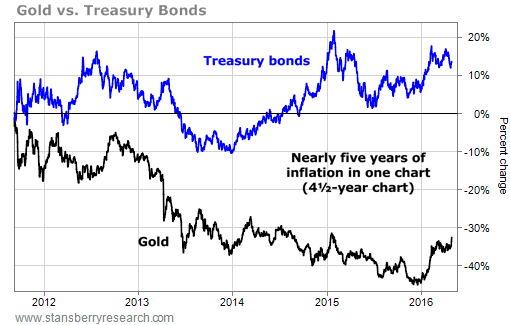

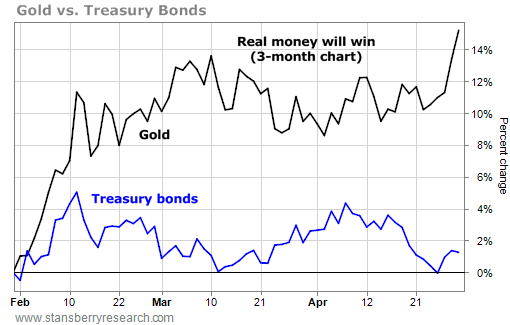

The next panic is about to begin… 'The beginning of the end'… Three facts you need to know right now… The next dominoes to fall… This isn't a typical Friday Digest. This isn't a typical Friday Digest.This is the most detailed and timely warning I (Porter) have ever written. I hope you'll take it seriously… I know most of you won't. Later, you'll claim that you didn't see it, or you didn't take the time to read it. But the truth is… you just won't be able to process the facts I outline below. And let me be clear: These are facts. What you'll find below aren't views or opinions. Or the ramblings of some mumbling oracle. I'm not talking about "Kondratieff waves"… or George Soros' aching back. These aren't hunches or guesses. I'm going to show you, in real time, how the entire system of modern, paper-based finance is coming unraveled. It's happening right now. And I believe the panic will start in May. In fact, I believe for decades to come, the summer of 2016 will be recalled as the beginning of the end… a period of grand financial catastrophe. So I hope you'll read carefully. But I'm so afraid you won't. When I began my career in finance 20 years ago, the world (defined as the G20 – the world's major economies) had about $40 trillion of debt. Today, the global economy has more than $230 trillion worth of debt.These obligations were not funded by patient saving, careful capital investments, a resulting gain to productivity, and increases to real wages and wealth. These credits were created, almost completely, by politicians and central bankers. The world's elite allocated this paper to achieve policy goals. The "invisible hand" of the market didn't distribute it. And it has resulted in massive, mind-blowing excess capacity in nearly every industry that's heavily financed, such as Chinese real estate development, the global automobile industry, U.S. higher education, and of course the oil business, which saw a massive ($500 billion-plus) injection of credit in just the last six years. What's important to grasp now is that these bubbles are not isolated – they are all connected, enabled, and continued through the coordinated actions of central banks. And these policies have reached their final "end game." The 20-year supercycle of more debt, lower interest rates, and one financial bubble after another has finally reached its climax.How do I know? Because the same policies that for 20-plus years have driven finance-related profits higher have now inverted. Lower interest rates, additional debt, and more manipulation have finally led to lower earnings for the world's biggest companies and banks. The volatility these policies have caused, the leverage that they created, and the resulting economic uncertainty are now all acting as a tax against prosperity. Every action in economics contains elements of diminishing returns. Economic stimulus is no exception. At some point, additional credit and lower interest rates can no longer propel an economy forward because the resulting overcapacity and overleverage cause more problems than they solve. Growth inevitably slows. Defaults inevitably rise.And… sooner or later… we'll see a panic. I believe that's happening now. Let me show you why. I've been writing about the relationship between gold and the U.S. long-term Treasury bond since around 2010.Think about these two financial instruments in these terms. On one hand, the U.S. Treasury bond is the monetary "brand" that stands for inflation, easy credit, and manipulation. Its value has increased, almost every year, in an almost linear fashion since the early 1980s. Gold, on the other hand, is an ancient monetary brand. The modern bankers say it's a "barbarous" relic. Gold stands for hard money, sound banking, and market-based interest rates. It is the bane of politicians and bankers. Since the peak of the last major banking crisis (the 2011 European "PIIGS" affair), gold has gone down 32%. An exchange-traded fund (ETF) that tracks "constant maturity" long-dated U.S. Treasury bonds (TLT) has gone up 13%. Tracked next to each other, the "spread" between the rising value of "banker's money" and the falling value of "real money" has widened significantly, and all in favor of the bankers… As long as belief in the central bank's ability to manipulate the markets and inflate financial assets remains intact, the value of the U.S. long bonds will rise and the relative value of gold will fall. But… when the turn comes… faith in the dollar will crumble. Faith in central bankers will evaporate. And the relationship between gold and the long bond will completely reverse. As long as belief in the central bank's ability to manipulate the markets and inflate financial assets remains intact, the value of the U.S. long bonds will rise and the relative value of gold will fall. But… when the turn comes… faith in the dollar will crumble. Faith in central bankers will evaporate. And the relationship between gold and the long bond will completely reverse.Here's that relationship over the last three months…  That's my first reason. The huge move in gold can't be explained unless you realize that the same people who have been manipulating the system for 20 years know the system is crumbling… and they're trying to get out. The huge move in gold is your most obvious sign. But it's not the only one… Another obvious sign is corporate profits. That's my first reason. The huge move in gold can't be explained unless you realize that the same people who have been manipulating the system for 20 years know the system is crumbling… and they're trying to get out. The huge move in gold is your most obvious sign. But it's not the only one… Another obvious sign is corporate profits.America's biggest corporations are a good way to judge the health of the global economy. When our best companies can't increase their earnings, we have a problem. For the last 115 years (for as long as we have reliable records), two consecutive quarters of falling U.S. corporate earnings led to a recession 81% of the time, according to investment bank JPMorgan. The only occasions that a recession was avoided were when there was a significant central-bank action to boost monetary stimulus. So how are our corporate profits doing now? The first quarter of this year marks the third consecutive quarter that saw a decline in U.S. corporate profits. And no, the problem isn't only a collapse in energy prices. The Wall Street Journal explains in detail…

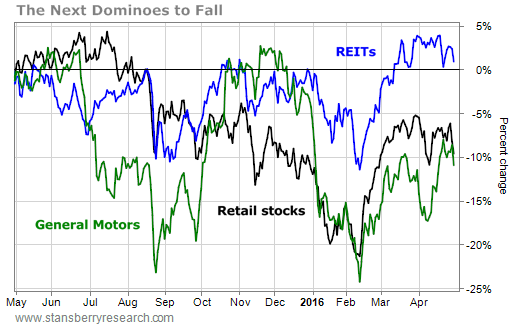

This decline in sales and profits might have been contained with aggressive central-bank action… but interest rates can't go any lower, not unless you want to start paying people to live in houses (through negative interest rates) and taxing people to use banks. If that happens, there's a good chance of sparking a global run on the banks. That's why I don't think you'll see negative interest rates much longer. And… there's a little-noticed bit of information about corporate earnings that I hope you'll recognize as being extremely unusual: Corporate revenues have now declined for five straight quarters. That's a longer downturn in corporate sales than during the 2008/2009 crisis.What's different now? The central banks have run out of bullets. They can't push any more money or credit into the system without causing bigger problems than they solve. In summary… the gig is up. The debt burden can't be carried any longer, not without causing overcapacity that destroys corporate profits. The wealthiest and most experienced investors in the world have long known this day would come. That's why they're expecting a collapse in the paper-money system. They're working on a way to bolster the U.S. banking system with a gold-backed dollar (see the "Metropolitan Plan"). The last month – with gold up big and Treasury bonds down – is a tiny prelude for what's coming. It's a sign… a sign few have noticed… I first began warning about the likelihood of a severe bear market in May 2014. I focused on the problems (the vast overvaluation) of the junk-bond market. I've been predicting a true catastrophe in the corporate-bond market ever since… and it has gone straight down almost the entire time. (And we've taken advantage of my prediction: All of our distressed-debt recommendations in Stansberry's Credit Opportunities have been profitable so far.) I still believe we're heading into a period of vast credit defaults, what I call "the greatest legal transfer of wealth in history." Likewise, I've been warning for a long time about the "lions" that I believed would lead to a bear market in stocks and the "deviants" that showed just how bad some of our debt problems had become. I'd like to add three more categories of stocks for you to begin tracking, to see if my fears about a massive bear market and monetary collapse are coming to pass. I want you to keep your eye on commercial real estate – as tracked by the Vanguard REIT Fund (VNQ)… the automobile industry – as tracked by General Motors (GM)… and the U.S. retail sector – as tracked by the SPDR S&P Retail Fund (XRT). The first two (commercial real estate and cars) are completely at the mercy of the credit markets. If we see a material reduction in the availability of credit, both of these industries will simply roll over… and the destruction will be immense. OK… but why now? Here's one reason: The price of used cars has begun to decline.Automotive sources indicate they expect used-car prices to decline by 5% or 6% this year – the first declines since 2008. Used-car prices are key to leasing rates and thus to the availability of credit in the sector. The amount of subprime lending that has happened in autos since 2014 means that price declines will be larger than folks expect and that credit losses will be much worse. At some point soon, the gaudy "earnings" that GM has been boasting about will be revealed to have been nothing but stupid lending and leasing to folks who can't afford new cars and trucks. Likewise, the U.S. consumer has been powering the global economy (thanks to a strong dollar and strong credit growth). Those trends are going to reverse, significantly, as our economy goes into recession. That will hurt the retail sector and, indirectly, commercial real estate, which always gets hammered during recessions and will get hammered doubly hard this time.Think about the amount of empty mall space. It's great that Amazon's (AMZN) earnings are soaring, but what that also means is malls are dying. Sooner or later, all of this empty commercial space will begin to hurt commercial real estate in general. Those malls are going to end up as office complexes and apartments… something nobody has figured out yet. Over the last five years (during the most recent boom), XRT shares are up 67% (compared to the Dow Jones Industrial Average's 39% gain). That outperformance is purely a function of credit expansion. Commercial real estate, despite the drag of mall space, is up 34% over the last five years. Only GM is down… because despite the massive credit expansion, there's simply far too much global overcapacity for automotive firms to make any genuine profit. These sectors are going to completely fall apart this summer. And you'll know why. So, what should you do with this information? Should you just go to bed scared tonight, but not change anything in your portfolio? After all, everyone knows you can't time the markets… So, what should you do with this information? Should you just go to bed scared tonight, but not change anything in your portfolio? After all, everyone knows you can't time the markets…As I've been telling you (for years), what's happening in our markets right now isn't normal. This isn't just going to be a "correction" or even a regular bear market. What's happening right now is the end of a massive credit expansion and a global experiment in paper money that is unlike anything we've ever seen before. Talking about these events as being an exercise in "market timing" is like folks on the deck of the Titanic talking about global warming. It completely misses the point. There have been periods in history – always after incredible credit inflations – when the markets themselves were destabilized to the point that there was nothing "efficient" about them. It's not that I object to the prices of stocks in the market. It's the global market itself that's broken. And if you don't think negative interest rates are the most "broken" thing you've ever seen in your financial life, you just aren't paying attention. By the way, it's not just some raving newsletter lunatic in Baltimore who sees a calamity approaching. David Stockman, the former vice chairman of private-equity firm Blackstone Group (BX), sees the same thing in the markets today. So does Carl Icahn, one of the greatest investors of the last 50 years. So what should you do? Please do something. Don't wait any longer. If you want to see if I'm right, wait until the end of next month. Stocks will be down big. Volatility will be up. And you will have lost a lot of money sitting on your hands. The essence of what you should do is simple: Raise cash, buy gold, establish some short positions, and ease into distressed bonds when they're trading at safe prices. (Warning: The last one isn't easy to do by yourself. Please consult our distressed-debt research inStansberry's Credit Opportunities before you try this at home.)Even if all you do is simply raise cash in your portfolio to 30% or 40%, I'm confident you'll beat the market this year. But… there's no reason you have to lose money at all. What's going to happen is a huge exchange of value… a legal transfer of wealth. And for our subscribers – who know what's happening, why it's happening, and how to profit from the situation – this year should be the best you've ever had as an investor. But you have to take action. And you have to do it right now. |

Regards,

Porter Stansberry

Baltimore, Maryland

April 29, 2016

No comments:

Post a Comment